Edited August 7, 2019: I have a follow-up post with more.

I’ve always had highly libertarian instincts, for both pragmatic and ideological reasons. You say civilians should be able to own rocket launchers, I demand that these rocket launchers not face a sales tax. But for me and people like me, the East Asian economic miracle poses a serious challenge: the greatest anti-poverty program in history involved not just a lot of capitalism, but a ton of state intervention as well. The history of East Asian economic growth in the last half of the twentieth century is a history of academics and the World Bank insisting that their policies couldn’t possibly work, followed by decades and decades of torrid growth.

So I decided to look into it. I read a few books (skip to the end for sources and recommendations), and learned a ton. As it turns out, though the Miracle is largely a triumph of capitalism, it also illuminates that economic growth depends on judiciously insulating certain parts of the economy from market forces.

In a way, you can look at success stories like Japan and South Korea as a different instantiation of two very American institutions: venture capital and private equity. The difference is that it was VC and PE as practiced by the state, rather than by individual companies; the timelines were longer, the plans were bolder, and the results were stunning.

No American company or investor has improved as many lives by as wide a margin as MITI, Park Chung-Hee, and Deng Xiaoping. But the methods are, at heart, startlingly similar: identify a critical inflection point, make a bold bet on an unproven market, “blitzscale” as quickly as possible, deftly react to crises, and carefully expose budding monopolists to hormetic doses of competition until they’re strong enough to monopolize on their own merits.

This is not just a theoretical exercise. An active trade policy has landed suddenly back on the policy menu in the US and other places. In the past, we’ve done it sort of shame-facedly, giving nice subsidies to Iowa in exchange for their tactically priceless supply of early caucus dates, periodically bailing out American companies when international exporters teach them the meaning of the word “competition,” and occasionally gesturing towards energy independence without putting any meaningful goals to paper.

But now we’re talking about trade in a more adversarial way, which is appropriate inasmuch as, in international trade, America has many adversaries — not places that hate us, just places that, as a side effect of their own policy goals, end up harming American economic interests. Of the many possible trade policies, most are bad and free trade is — on net, and in the aggregate — the best. However,the simple Ricardian model of trade makes a few untenable assumptions, and other countries have learned to exploit them. In the spirit of free inquiry and open debate, I am happy to explain why anyone who advocates either contemporary protectionism or contemporary free trade is wrong.

But we’ll have to start at the beginning: how did East Asian countries get so rich, so fast?

Origins: How Did the Boom Start?

I’d like to begin by rehabilitating another long-since discredited economist: you can’t really understand the Miracle until you learn to think like a Malthusian. Malthus’s original thesis was that since population grows exponentially and food production grows linearly (with some deviations), we’ll always tend to grow the population to the point that maximum food output can just barely support it, meaning that a single bad harvest leads to famine.

Granting the premises, this is true, and looking back at history, his premises arguably made sense. Populations had gone through boom/bust cycles before, albeit more driven by war and disease than by famine per se — but war and disease are both symptoms of overcrowding, so the model was predictive even though it mislabeled the terms.

Of course, the two mistakes he made were the two premises: as it turns out, food production can grow exponentially, while population growth slows as countries get richer and better-educated.[1] One important thing to keep in mind when you’re thinking like a Malthusian is to note that if your country is close to the Malthusian limit, it means the incremental farmer is not producing enough food to feed themselves — if the average person produces enough food for one person, and some people have good land, the more marginal land is necessarily producing less than that average. That’s important because the non-farming population is able to accumulate capital, which can eventually raise farms’ efficiency, at least on a per-farmer basis. While farmers invent a ton of stuff, they can’t manufacture at scale.

So the story of Western Europe, starting at around when Malthus published, went like this: Farmers produced enough resources to support some basic manufacturing; this manufacturing produced capital that made farms more efficient; fewer farmers required meant more manufacturing, setting off a virtuous cycle.

Arguably, the event that set off the Renaissance, and thus the Industrial Revolution, was the Black Death. By killing a third of Europe, it pushed us to well below the Malthusian limit, raised workers’ wages, and limited governments’ ability to tax city-dwellers. Things really started to take off in Northern Italy, which is also where the plague first arrived. Of course, it could have happened anyway, and could have happened elsewhere — the reason it hit in the first place was that trade had globalized enough that rats and fleas from China found their way to Venice, which wasn’t happening as much beforehand. But certainly the Bubonic Plague accelerated things by eliminating a lot of people and raising the marginal productivity of the survivors.

For countries that didn’t have Europe’s good fortune in getting a catastrophic plague right when their technology had advanced to the point that they could rapidly scale up non-agricultural productivity, there was some more waiting involved.

As Joe Studwell points out in How Asia Works, every one of the economic miracles started with land reform — in Korea and Japan, this was part of a series of postwar changes; in China, it happened a little later with the gradual rescission of agricultural collectivization.

Land reform’s effects were paradoxical: in the short term, the net effect was more agricultural labor. Individual farmers intensively working small plots can achieve much higher productivity per acre than big plantations can, at the cost of not being very scalable. But for a country on the edge of the Malthusian trap, that’s exactly what they need.

What happened next, in every successful case, was that governments decided as a matter of policy that they’d favor export industries, and in particular that they’d favor industries that could achieve long-term productivity growth. In some ways, these countries lucked out due to the Green Revolution: if agricultural productivity in general hadn’t started to rise, they would have been stuck at a slightly higher Malthusian limit.

In each case, the first inflection that set off the boom was land reform. After that, two things happened: First, each country had a trade surplus, and the smart ones invested it in capital equipment for stage two. Second, birthrates rose. Since they had previously been bumping up against the Malthusian limit, an increase in food supply led directly to an increase in babies.[2]

For policymakers, the name of the game is this: you have some hard currency, and some babies. In seventy years, these babies will retire, and the next generation may well be smaller. What do you do in 1950 to ensure that the retirement accounts of 2020’s 70-year-olds are as full as possible, so they can soften the impact of a high dependency ratio?

The process:

- Invest the trade surplus from food into light industry, i.e. textiles — this is a business where the main input is unskilled labor, so any poor country with a port and a smidgen of capital is, presto, the global low-cost leader.

- Invest the trade surplus from that into heavy industry (at first: steel and basic chemicals; eventually heavy machinery, cars, specialty chemicals, electronics).

- Relentlessly push your heavy industry to export; sell products that can compete globally, even if you’re taxing your population to subsidize your exporters.

- On that note: use aggressive financial repression; force people to save a high proportion of their marginal product (i.e. standards of living can rise, but should rise a lot less than GDP); direct that money into industries with economies of scale.

- Once you are the scale leader in a scale-driven industry, you can relax. But only a little! Now you have to worry about somebody else copying you. Japan’s world-beating steel industry got copied by South Korea, and their car industry faced competition there, too; Japan also lost their lead in electronics to China.

Case Study: Japan

Postwar Japan was an economic basketcase. The country had lost over two million lives, and American bombings had wrecked their industrial capacity. Even before that, Japan’s militarist government had warped the country’s economic development through a focus on arming for conquest.

As a consequence of all this, Japan’s GDP per capita in 1950 was under a fifth of the US level. Today, Japan’s GDP per capita is about two thirds of the US level.

When you try to evaluate the Japanese system, it’s important to note that it does not at all work the way it looks on paper.[3] In theory, Japan is a representative democracy, in which voters elect legislators who pass laws, etc. etc. etc. In practice, their system during the last half of the twentieth century was a sort of technocratic dictatorship, in which the foundational rules were not a written constitution but a set of bureaucratic social norms.

The protagonist of Japan’s industrialization is the Ministry of International Trade and Industry, which determined Japanese industrial policy. In the US, we’re used to thinking of government bureaucracies as slow and unambitious, but in Japan that wasn’t the case at all: MITI got the country’s best workers (the pass rate for their most challenging exam was 2%), and had an aggressive up-or-out approach. Talented people quickly got more responsibility, and they wielded immense power.

When MITI decided that Japan should be a steel exporter, they gave steel companies enormous loans to increase capacity. When the industry got overbuilt, MITI forced participants to merge. Since steel had economies of scale and was a useful input for other kinds of manufacturing, MITI decided that so if Japan were to have a future, it would start with steel.

And MITI was right. Japan became the world’s largest producer of steel by the early 80s, and their dominance in steel gave them a huge boost in shipbuilding and machinery.

Here are three striking illustrations of how powerful MITI was (one political, one sociological, one cultural):

- Japanese legislators could introduce their own bills, but these tended to get voted down. MITI could also suggest bills, which tended to get passed with near-unanimity. That Japanese Diet in the postwar period looked less like the US Congress than it did the Supreme Soviet of the Soviet Union. Once the legislators saw the bill, it was as good as law. In MITI and the Japanese Miracle, Chalmers Johnson argues that this was an efficient system because the legislators “reigned” (they were the public face of government, and enjoyed the electoral consequences of policy decisions) while bureaucrats ruled (i.e. they made the actual decisions).

- A study of the family trees of prominent Japanese people showed that high-level MITI employees tended to have more socially-prominent fathers-in-law than fathers. MITI, in other words, was where ambitious and upwardly-mobile young men wanted to work. Why bother getting rich when you can get powerful instead?

- There are no fewer than three novels about Shigeru Sahashi, a powerful MITI vice-minister. One of them got turned into a TV show. Imagine The West Wing, but the hero works at the Department of Commerce.

MITI seems to have had a work-hard/play-hard culture. The MITI cliques tended to center around senior employees who were generous with their liquor cabinets. After a grueling fourteen-hour day of designing and implementing industrial policy, how better to relax than to throw back some Suntory and spend a couple more hours… discussing industrial policy?[4]

Senior employees did get rich, through a tradition of Amakudari (“descent from heaven”) in which senior bureaucrats would, late in their careers, land C-level jobs at the companies they had regulated. In an American context, the assumption is that this sort of revolving door becomes a way for a company to buy influence, but in Japan it appears a bit different: Amakudari offered a way for bureaucrats to ensure that their recommendations were being implemented. (And to finally get a nice company car, of course.)

The Japanese industrial growth playbook, for industry after industry, looked like this:

- Bureaucrats would pressure banks to make loans and pressure companies to add capacity.

- They’d subsidize companies based on export volume — in other words, a company didn’t have to be profitable, but it did have to compete.

- As companies scaled up, the subsidies dialed down. Sometimes this was due to international pressure (although they were adept at dodging that; when Japan finally stopped directly subsidizing exports, they started allowing exporters to depreciate equipment faster, which, for a profitable company, is economically equivalent to a direct subsidy).

- Once the industry reached viable scale, they’d rationalize capacity — merge competing firms, shut down inefficient plants — and move on to the next.

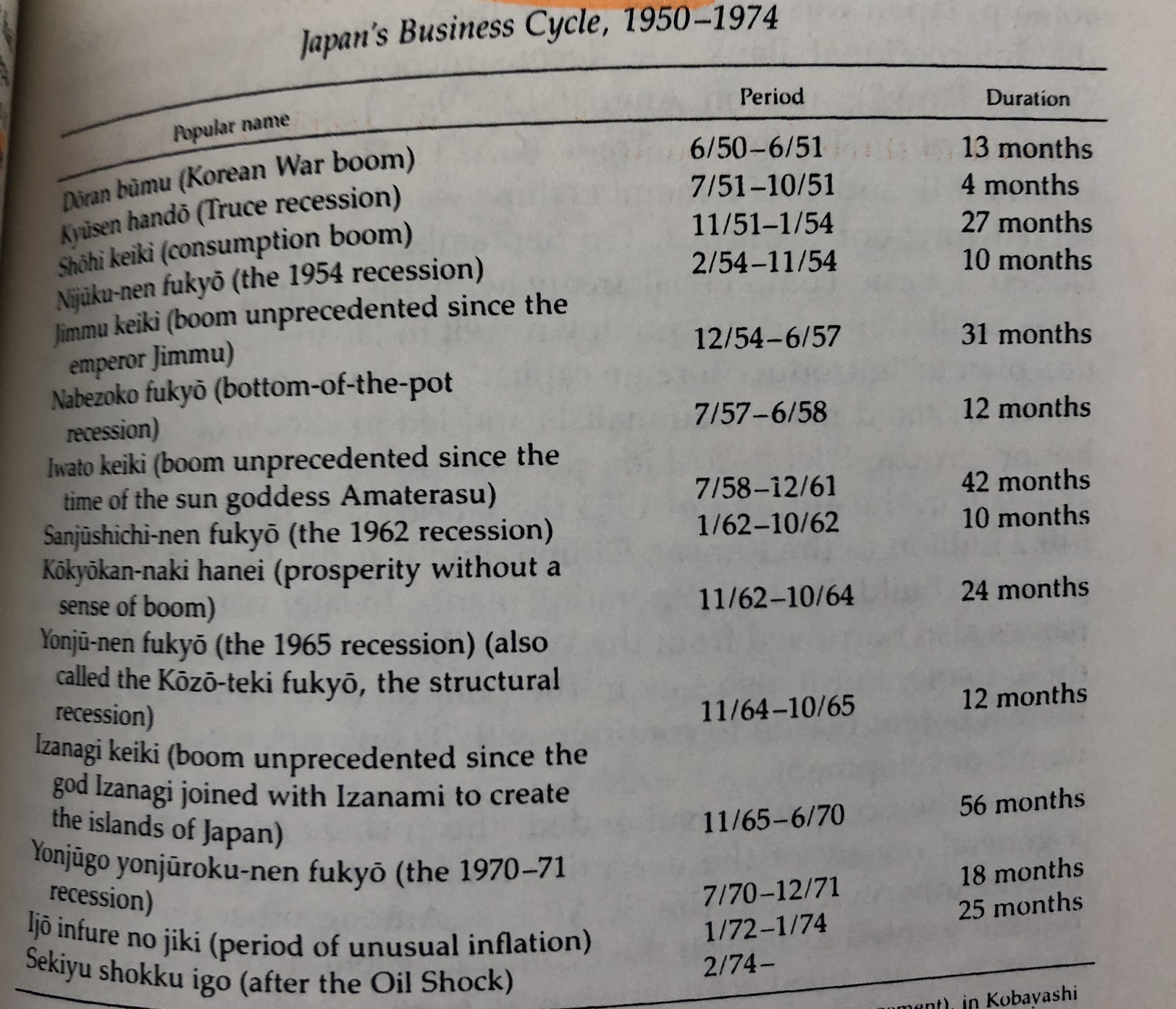

Japanese postwar economic history was a long series of increasingly impressive export-driven economic booms, leading to a serious level of creative nicknames:

And then, in the 80s, things got crazy, and in the 90s things fell apart.

The denouement of the bubble is an instructive example of the limits of policy interventions: Japan was basically forced to stop artificially devaluing their currency, which led to a property and asset bubble, and then a long period of economic stagnation. Demographic collapse didn’t help — instead of benefiting from a baby boom, Japan faced a growing population of elderly people, who tended to sit on their savings even at zero interest rates. (The current yield on Japanese ten-year government bonds is -0.04%.)

But still, Japan is a rich country; growth may be slow, but “growth” is the first derivative of GDP, and their GDP is quite impressive. For most of its history, Japan was a poor country. After a few decades of aggressive industrial policy, it became a rich one. And while it’s not the richest it’s ever been, that’s not the metric that matters.

Case Study: South Korea

South Korea’s economic growth is basically a gritty reboot of Japan’s story. Japan was a technocracy disguised as a democracy; South Korea was a poorly-run democracy until a major general decided that the votes that mattered were from the people with guns.

South Korea was poor, like Japan — only poorer. They’d survived a war, like Japan — but in their case, they were invaded by a nuclear power, and with the help of another nuclear power they fought back to a stalemate. Japan is surrounded on all sides by water; Korea was mostly surrounded by enemies.

And yet, they got rich. As recently as the 1960s, South Korea depended on US aid to avert famines. Not only do they now export lots of steel, chemicals, cars, and phones, but their single biggest cultural export is an incredibly catchy song about the spiritual agony of living in a wealthy country.

There’s a sort of Girardian side to South Korea’s industrialization story: Park Chung-Hee’s attitude towards Japan was 1) idolizing their success, and 2) fiercely committing to destroying them. Park was educated in Japan and served in their military; as President he would sometimes stay up late reading books about their economy.

Would you buy millions and millions of new cars from this man?

The South Korean industrialization story kicks into high gear with the foundation of their steel company, POSCO. Korea needed money and expertise to build a steel plant, and they got both — from their historical enemy, Japan, in exchange for accepting a Japanese apology over colonialism. This is the kind of decision a popularly-elected leader can’t afford to make. Park Chung-Hee only did it because he believed that it was the right choice (and that tanks matter more than votes).

POSCO construction crews were reminded that the plant was built with Japanese war reparations, and that it was a matter of national honor that Korea supplant Japan — specifically, the foreman allegedly suggested to employees that if they couldn’t hit their deadlines, they should consider suicide.

From there, Korea expanded into chemicals, and, famously, cars. Like Japan, their government put immense pressure on banks to lend to manufacturers, and on manufacturers to sell abroad. And, like Japan, Korea depended on a loyal cadre of highly effective bureaucrats. Korea benefited from a side effect of being ruled by a military junta: the Korean military under Japan was the best-educated segment of society, so once they ran their own show, they did it well. Interestingly enough, Korea’s civil-service exams had a 2% pass rate — exactly the same as Japan’s. There were only a few good schools, so most of the senior bureaucrats developed strong social ties — good for coordinating plans, but bad for admitting mistakes.

Because the challenges facing South Korean were more dire, its actions were more extreme than those of the Japan: at one point, Park Chung-Hee nationalized the banking system and imprisoned the heads of most Korean chaebol conglomerates, suspecting that they were hoarding cash. (As it turned out, they weren’t; he let them go and loosened controls on the banks soon after.)[5] Park insulated bureaucrats from the political consequences of their actions, which allowed them to think further ahead than typical government employees. Under a corrupt system, that would be a disaster butunder an efficient one, it was a boon.

The repeating pattern in South Korea’s growth was that exporters would borrow enormous amounts, over-expand, then lose lots of money and be forced to merge or go under while the government scrambled to get enough foreign capital to pay the bills. This system can’t last forever, but it’s basically running an industrial policy by making a series of Kelly bets: you maximize your long-term returns only by accepting a surprisingly high level of volatility.

This also explains some of South Korea’s otherwise bizarre foreign policy decisions. South Korea was the second-largest contributor of manpower to the Vietnam war, sending about five times as many troops as the #3 participant, Australia. This was a geopolitical bankshot: the point was not to keep South Vietnam capitalist, it was to guilt American troops into staying in South Korea.

South Korea’s policies under Park Chung-Hee make sense as an effort to address the existential risk of invasion by the North. This remained a live risk for his entire tenure; North Korean commandos regularly made incursions into South Korea, and they were likely involved in an assassination attempt that took the life of Park’s wife. This also explains Park’s repressive domestic policies — the Park regime brutally suppressed student protestors and labor unions. Their human rights record was not exactly enviable, but given the situation they faced it becomes somewhat understandable.

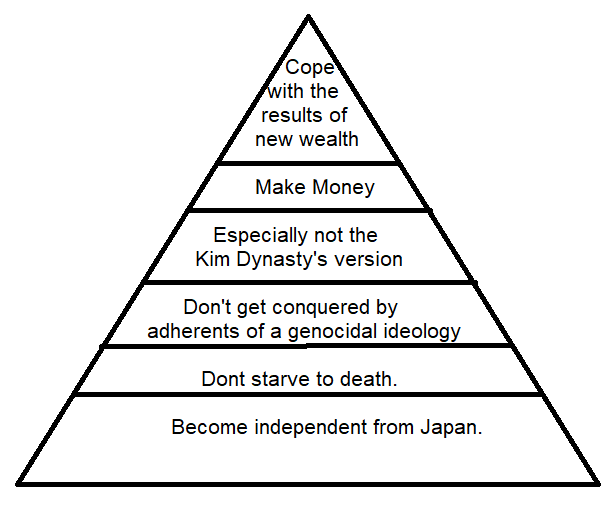

Here’s a Maslow’s Hierarchy of Needs for South Korea:

Park did not adhere to democratic norms, although South Korea eventually adopted a fairly representative system. What Park had instead of popularity was legitimacy, which I’d define as when society gives you permission not to ask for their permission. South Korea’s industrial policy was a series of high-risk, unpopular decisions, of the sort that would have been voted down by gigantic margins in any representative system. Fortunately for today’s Koreans, such a system didn’t exist: Park and his junta decided that they were the right people to run things, figured out what to do, and did it.

Singapore and China: The Missing Case Studies

If I’d written this piece before reading How Asia Works, I would have spent a lot of time on Singapore: it exemplifies the approach of using market signals for implementation but maintaining state guidance. Singapore also used a much more free-market approach than other countries. But, as Joe Studwell argues, Singapore and Hong Kong are not useful case studies, because free market policies work unusually well for city-states that prosper through trade and finance. If you have a port, and your port is close to a growing industrial powerhouse, you don’t have to plan ahead as much; you just have to avoid making any catastrophic mistakes. Singapore did exactly that, in fact; thanks to their government’s policies, they’re a lot richer than they otherwise would have been. But they’d still counterfactually be pretty rich, just by virtue of how much cargo and capital passes through their general vicinity.

Lee Kuan Yew gets a lot of mindshare for the same reason Churchill does — say what you want about his decisions, but he probably said it better in one of his books. LKY has a particular gift for gently making fun of American elite opinion, as if he’s just been cheered up thinking about how the American Cambridge houses even more eccentrics than the English one.

Singapore’s position as a port city in the general vicinity of several rapidly-industrializing countries meant that it could pursue truly laissez-faire policies and expect good results. Of course, the state intervened heavily in Singapore (it’s odd that such a capitalist paradise has most of its citizens living in government housing), but Singapore is an order of magnitude less economically intrusive than the other case studies.

It’s hard to prematurely optimize a port or a financial hub. You might somehow get an edge by knowing what raw materials are cheap to ship there, then assembling them and exporting, but touching the supply chain at only one point makes things tricky. At the same time, a city-state like Singapore does have the advantage that it’s relatively easier to maintain control, which means the government can tolerate more macroeconomic volatility, and that means that they can better afford to pursue to the monetary stability the IMF loves so much.

The math is just different when your riot police can walk across the entirety of the country in under an hour. The lesson of Singapore is that it’s good to have a port, and if you have one, your job is a lot easier.

In China, we have the opposite problem: if Singapore is hard to use as an example because it’s small-scale and doesn’t need to control its own destiny, China is hard to talk about because everything that happens there happens on such an enormous scale — and because, unlike the other countries I’ve discussed, China’s leaders see it playing a globally hegemonic role in the future. At one level, of course, they’d like to have a rich country because it’s nice to be rich. But at another level, they have manpower and want a similar amount of materiel.

This is important, because economic development in most countries has a more boring endgame: economically, most people want to live in 1950s America. China has different plans: yes, they want their workers to be rich — rich enough that they can take a vacation to Taiwan and visit landmarks like Xi Jinping Plaza and the Victims Of Kuomintang Atrocities Memorial.[6]

China is also hard to analyze because the anti-capitalist faction won their civil war, and capitalism only came back once those winners finally died. While their policies from the 80s on show a substantial amount of foresight, they didn’t need quite as much as Korea or Japan, because those countries had already done the hard work. Japan had to adopt ideas from 19th century neo-mercantilists, and Korea had to adapt them, but China just had to look at what had worked over the previous decades and do it at scale.

China also benefited from a rising tide of globalization. Their economic growth really kicked into high gear once they joined the WTO, especially since they were willing to drag their feet on issues like IP theft and protection. More so than the other case studies, China managed to implement a system of free trade for thee and protectionism for me, and use it to achieve dominant scale in industries with impressive economies of scale. Their plan seems to be to keep on doing this, with more and more industries, unless someone stops them. In Internet meme terms: if you’re at the top of a meritocracy and you rule for life, plus everyone you negotiate with is an elected official with a term limit, you’re a player character going one-on-one with NPCs.

Why These Techniques Work

Japan and Korea implemented similarly heterodox policies and saw similar levels of success. It’s worth looking at how some of these techniques worked in practice, and how they fit together. After that, I’ll address the implications for the US today.

Export Subsidies: Y Combinator for Steel

Export discipline is the single most powerful concept behind the East Asian Economic Miracle. The idea is simple: the only way to produce wealth is to make something people in other countries want to buy, but poor countries have a comparative disadvantage in complex manufacturing. The solution that worked for Japan, Korea, Taiwan, and China was simple: protect and subsidize exporters, but only subsidize them to the extent that they can actually sell something in other countries.

The car industry has punishing economies of scale. You need to design vehicles, source parts, and actually build them, and the minimum cost to do this is prohibitive. If you build one tenth of General Motors, you don’t earn one tenth of what GM does. Instead, you lose a lot of money, because you have a sub-scale factory that’s producing well below capacity.

But the counterpoint to that is that if you build something twice as big as GM, you’re going to make more than 2x what GM does, which means your incremental returns on capital are far higher. GM, at least in the mid-twentieth century, was mostly selling cars to Americans, and America was the land of abundant capital, high wages, and cheap oil — all of which were de facto subsidies for domestic auto demand. But those implicit subsidies applied to imports just as much as domestically-produced cars, so the industrial planners knew that if they achieved breakeven, they’d enjoy a long runway during which they’d produce higher returns.

One way to look at export subsidies is that, like in The Producers, they let a company sell more than 100% of its equity. In this case, the government is essentially “short” the exporter’s profits, and distributes the corresponding long position to the company’s management and the banks that finance its expansion. By ensuring that the people with a stake in the outcome are the ones who can make a better outcome happen, they align incentives towards growth.

This is a centralized, government-based riff on exactly the same logic as venture capital. VC also provides bridge financing to subsidize some behavior that’s unprofitable at small scale but very valuable at a larger scale — export discipline from MITI is economically equivalent to VCs who will fund a negative cash-flow business as long as it has high gross margins, low user churn, and network effects.

There are a surprising number of parallels between these policies and the way startups work:

- Startups often sell to other startups at first. Salesforce did this in a big way; Y Combinator is a sort of Zaibatsu that gives startups instant access to a few hundred good customers.

- Below-market salaries and big options packages make employees hard to poach, mimicking the effects that lifetime employment and government-sanctioned monopolies have on employee incentives.

- Small group of people has no politics. Ten people working on a project is pretty apolitical. Fifty who come from the same extended social network and also share the same crazy mission will also be fairly apolitical.

- There’s no immediate need to turn a profit, but intense need to show growth. A startup that gets valued at 30x sales in one round and 5x sales at IPO has a similar cadence of external cashflows to a steel company that starts out getting 50% of its revenues from export subsidies and matures with 95% of its revenues from real customers.

Essentially, these planners were building an industrial base for a future in which they’d be about as wealthy as the Americans. Japan, they knew, would eventually become a country where lots of people wanted to buy cars, radios, and appliances, and the best way to sell those domestic consumers quality products was first to compete for the wallet-share of the wealthier and pickier American and Western European consumer. Even today, Japan’s auto industry is implicitly and explicitly subsidized. As The Economist points out, Japan mandates expensive safety tests for cars after three years. Rather than pay for the tests, many consumers sell their used cars and upgrade to a newer model. Result: everyone in Ulaanbaatar drives a Prius.

Inflation: When It’s Not So Bad

The IMF is notorious for telling countries not to let inflation get out of control, and developing markets are equally notorious for bouts of severe inflation. Korea went through years of high-CPI growth, Japan had extreme inflation early in its development, and of course other developing markets to this day go through cycles of elevated inflation.

The argument against high inflation is straightforward: it makes it hard for investors to feel confident in the value of their assets, especially fixed-income assets. If you’re an ambitious technocrat, your country needs to issue lots of bonds, and your country’s banks need lots of foreign capital flows as well. High inflation makes that difficult.

The pro-inflation argument is a lot simpler: inflation is a side effect of fiscal or monetary stimulus, both of which accelerate growth.

In the case of the Miracle economies, demographics and cultural norms conspired to make high inflation an unusually prudent policy. For reasons that may never obtain again, the policies that South Korea pursued (which led to 10%+ inflation throughout the 1960s) were actually quite prudent. Japan’s inflation, a more modest mid-single digit rate during that time period, was also quite acceptable.

What both countries benefited from was the combination of:

- Population growth driven by agricultural reform, which helped them escape the Malthusian trap and expanded family sizes (South Korea’s population grew by 2–3% per year throughout the 60s).

- A set of cultural norms that strongly encouraged young people to support their parents.

If mom and dad’s pension loses 80% of its value in real terms, but your wages rise 4x over the same time period, it’s no big deal — your salary was their retirement plan all along anyways. Essentially, these countries could use families as an intergenerational redistribution mechanism, meaning that they only had to care about the aggregate change in the net present value of incomes, not the distribution thereof.[7]

As those same countries lapped the impact of their baby booms, and started seeing low-to-negative population growth, they faced harder policy decisions. Fiscal stimulus dilutes the net worths of old people on fixed incomes, and those people vote. Meanwhile, monetary stimulus tends to help them, which pushes East Asian economies towards zero interest policies.

Corruption: Also Not So Bad

Samuel Huntington has a very illuminating line about corruption:

“In terms of economic growth, the only thing worse than a society with a rigid, overcentralized, dishonest bureaucracy is one with a rigid, overcentralized, honest bureaucracy. A society which is relatively uncorrupt — a traditional society for instance where traditional norms are still powerful — may find a certain amount of corruption a welcome lubricant easing the path to modernization.”

Call it Coasian corruption: you accept some level of bribery because the people who expect the best returns on investment are the ones willing to offer the largest bribes, and you can’t easily write the rules in advance (while you can retroactively refine them). In a sense, corruption provides a valuable signal: if your country’s senior automotive bureaucrat lives in a mansion while the most important steel bureaucrat lives in his parents’ spare bedroom, maybe steel isn’t your country’s most competitive export.

All of the Miracle economies have had corruption problems, but they often seem to be a side effect of wealth creation. After all, something can only get stolen if there’s something to steal.

Like inflation, a surprisingly high level of corruption is tolerable in the short term, but eventually becomes a problem. While it’s hard to measure, the real heuristic is this: corruption is prosocial in a developing market when it helps skirt rules that discourage wealth creation. It becomes a problem when the prospect of corruption encourages rules that stymie growth.

In China, a major source of corruption is the sale of land. Land is, in effect, owned by local governments, who must sell it to pay their expenses. And land in China is quite valuable. Naturally, many land purchases involve consulting fees paid to offshore companies that happen to be controlled by the immediate family members of the people in charge of deciding which factory owner gets which plot of land. If the result is that factory owners competitively seek out the best places to build new plants, and start construction as quickly as possible, then it’s a net boon to Chinese growth. But it’s also a signal that the land-sale system needs to get formalized.

China has passed the point at which additional corruption lubricates rather than retards growthThey may have reached the dangerous point where crooks are sufficiently entrenched such that they can’t be easily dislodged. But Japan and Korea have had massive bribery scandals in the past while continuing to grow right through them, so while this is not ideal it’s hardly catastrophic.

As the economy matures, of course, it does get catastrophic. You can take the converse of Huntington’s argument: if corruption is helpful when the rules don’t make sense, it’s harmful when they do. At 10% GDP growth, any government policy runs the risk of being obsolete by the time it’s implemented; at 2% growth or 0% growth, that’s no longer the case.

IP Piracy: Great Artists Steal

One good business model is to spend a lot of money upfront to produce some fantastic new technology, and then sell a unique and high-margin product based on it.

For an even more profitable model,skip the expensive R&D and just copy somebody else’s work. This is a time-honored tradition; as Ha-Joon Chang points out in Bad Samaritans, Renaissance England once had comically aggressive industrial espionage laws (if you told the perfidious Dutch the secrets of English textiles, you could be executed).

This practice is ubiquitous — China is famous for technology-transfer deals today, but Japan did exactly the same thing to IBM and the car companies a few decades ago, as did Korea. The defense of it is a kind of quirky utilitarian argument: it’s not like Japan was going to buy very many IBM mainframes or Cadillacs at full-price in 1960, so the existence of cut-rate copies is no great loss.

Both Japan and Korea significantly dialed back the IP theft as they advanced, and started doing their own R&D instead. Today, there are many industries where the US would benefit from filching East Asian IP — but, of course, we don’t have governmental air cover should we attempt to do so, and Japanese and Korean companies are not especially excited to invite American engineers and researchers over to tour the lab and learn their secrets.

China, on the other hand, has not pulled back. As a result, they’re facing the consequences that Japan and South Korea were able to avoid: the inability to cooperate with R&D efforts at American and European companies, and retaliatory trade actions.

This strategy is not, of course, unique to industrial policy. Basically any online community that allows user-generated content will benefit from allowing users to generate lots of content by pirating it. The usual model is that you slowly crack down on the stolen stuff, and grow your legitimate business to the point that when you do finally pay a fine or settle a lawsuit, you’ve grown your way out of the fine. If you get fined 100% of your revenue for allowing piracy, but you grow your business 10x by the time you actually pay the fine, you’ll survive. Perhaps China’s planners are performing exactly the same calculation.

Financial Repression

Successful industrializers use a broad array of tactics to raise the savings and investment rate in their countries.

I should emphasize three things about this regime:

1. It’s unpleasant for the people who live through it.

2. It’s nice for their descendants.

3. I don’t want to be the kind of person whose descendants grumble that all that consumption must have been fun for you, dad. Better to have kids who know that you’d chew broken glass to build them a better future.

The two basic levers for financial repression are encouraging saving and discouraging consumption. Most industralizers use high tariffs and capital controls to keep people from consuming.

Direct tariffs work as a means of reducing local consumption, but trade treaties often preclude them. Fortunately for savvy countries, there are ways to apply indirect tariffs, too. Japan has a large wholesale industry: according to Johnson’s MITI, in the late 60s, Japan’s wholesale sector generated almost 5x the revenue of Japanese retailers, compared to a 1.3:1 ratio in the US. This oversized wholesale industry served two purposes: it was a welfare/retirement program for unneeded workers in manufacturing companies, and it meant many layers of red tape for companies exporting to Japan. If every middleman charges foreign companies just a little bit more, the total “middleman tax” is raised to the power of the number of layers of middlemen.

One of the important levers Japan and Korea pulled was on the savings side: by reducing people’s opportunities to spend money, they forced them to save, and both countries artificially reduced interest rates on deposits, generally to below the rate of inflation. In other words, savers were literally paying banks to hold on to their money.

Why did savers do this? It’s unclear whether this was an explicit goal or a lucky accident, but macroeconomic volatility coupled with a weak safety net for individuals places enormous pressure on people to save money. If you don’t have unemployment insurance or welfare, and your friends and family are all desperately poor, you need to rely on your own savings if you get laid off. High GDP growth gave people enough money to save, and the risk of a recession gave them an incentive to.

These savings constituted free money for banks. In return, the state required banks to make uneconomic loans. In a poorly-functioning system, this would have the inevitable result that either banks would avoid taking risk, and just collect the profits on their cheap deposits. Or they’d make loans to well-connected borrowers, rather than to the companies that represented the best prospects. In a system where ambitious people work in the private sector or legislature, that’s exactly what would happen — it’s exactly what does happen, even in developed countries with stable institutions, like the US. But in the Miracle economies, the most ambitious people were the ones telling banks where to lend, not the ones doing the borrowing or the lending, or taking political credit for the jobs that resulted.

Financial repression is redistribution from individuals to big business, but in a less individualist country, “big business” is something closer to “national wealth held in trust.” So it’s really redistribution from present consumers to future consumers. This is also unfair! Utilitarians would be aghast at the idea of taking money from the poor and giving it to the rich, and in global/historical terms, the Japanese in the 50s were poor while their present descendants are rich.

Banks Over Bonds

James Carville liked to tell a joke: “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.” Markets are great at allocating resources, but they’re often quite reactive. Carville was right about that: if bond investors are mad, you’ll know about it. As a result, any business or country that relies on capital markets for funding faces immediate consequences if it doesn’t follow those markets’ conventional wisdom.

The alternative is to source capital from banks: bank loans don’t get quoted every day on an exchange, so even if something reduces the loan’s perceived odds of getting repaid, accounting rules allow bankers and borrowers to live in denial. This later turned into a huge problem in Japan, Korea, and China; all three countries suffered from zombie banks that financed zombie companies, while in a more open market the result would have been bankruptcy. But during the growth phase, a banking system can grow its way out of early problems.

Growing out of one’s problems is generally an imprudent strategy. That’s what burned the S&Ls and junk bonds in the 80s, and it’s been the bane of consumer lenders and insurers for longer. But since the Miracle economies focused on industries with economies of scale, growing out of the problem really did work. Korea forced its marginal auto manufacturers to merge or shut down, but the survivors can service their debts.

Banks have another advantage in a country with a well-run government that can ignore near-term popular pressure: they serve as a more direct conduit between fiscal/monetary policy and economic behavior. When MITI or the Korean industrial planners decided that their economy needed a little more juice, they ordered banks to lend more, which immediately resulted in higher capital expenditures and quickly added jobs. A bank-based system, in other words, means there’s a direct conduit from a central bank’s lender-of-last-resort status to balance sheets, companies, and workers. Savers get dinged by this, but the logic of financial repression holds: savers are saving because of the risk of macro instability, so diluting the inflation-adjusted value of savings while cushioning the blows from a recession can be a wash, or even a win.

A system like the US Fed has to operate more indirectly, by tweaking short-term risk-free interest rates in the hope that this will propagate through the entire rate curve and affect credit spreads in a predictable way. I’m sure Bernanke would have liked to just order every bank in the US to lend lend lend until the vaults were empty. When short-term rates hit zero, central banks have to intervene more, but in a US and Western European context they prefer a shotgun approach to a sniper rifle.

Policy Implications for the US

As a capitalist, I believe everyone has a right to try to get rich. As an American, I welcome their efforts to do so, at the expense of any country but one.

As we’ve seen, the policies pursued by the Miracle economies produced better results than are implied by classical economic theories. That observation doesn’t invalidate the theories, it just illustrates their limitations: “If X and Y, then Z” implies “If not Z, then not X or Y.” Good candidates for X or Y include perfect competition and constant returns to scale.

In a Ricardian model, a country should always focus on whatever it has a comparative advantage in. The model that works is to focus on what you could have a comparative advantage in, and do whatever it takes to get that advantage.

Considering this, what limitations does the US face in responding to these policies?

Our government employees are not high-status, and there’s not a clear path to making them so. The recent shutdown a striking case in point. This Vox piece summarizes the standard view of the shutdown’s adverse consequences. 800,000 people were furloughed from their jobs. The concrete results Vox talks about are from how they spend their money. It’s assumed that the marginal productivity of the 800,000 least essential government employees is zero; there isn’t anything they’re supposed to be accomplishing other than cashing paychecks.

Granted, the shutdown did cause inconveniences, but these nearly always fit the same pattern: “This is illegal unless specifically approved, and the person responsible for approving it has been deemed inessential and is not at work today.”

I don’t mean to imply that all government employees are completely ineffectual, just that being ineffectual is not a bar to continued employment. The most predictive model of the modal government employee in the US is that they’re collecting a pension from day one, but they have to wait in line for roughly forty hours a week to receive it. Fortunately, they can entertain themselves while waiting.

Japan, China, and Korea all benefited from a long tradition of high-status civil servants. Korea and China had a government strongly influenced by the military (in Korea because the military seized power; in China because the military wing of the Party conquered the country.) In both cases, they traded off their recent record of military success. The US military isn’t going to match that level of status any time soon. While it’s an incredibly impressive organization in many ways, it’s been a long time since we’ve had a morally and strategically unambiguous victory.[8]

Our deep capital markets make it hard for the government to direct capital to strategically important industries, but given the status gap that’s a good thing. If the smartest and hardest-working people are in the convincing-bureaucrats-this-is-a-strategic-imperative business, the result will be that any business that can absorb a lot of capital and employ a lot of smart people will benefit.

Robust capital markets make it hard to hide short-term pain. If the loans backing POSCO or the South Korean chemicals industry had been traded on open markets, they might have dropped from 100 cents on the dollar down to 50 or less as the project struggled to take off. But on a bank’s balance sheet, a loan that hasn’t defaulted yet can be marked to 100, 100, 100, every year, for as long as necessary.

This is not strictly a disadvantage. It means the American system is great at pruning dead wood. We don’t make very many televisions, shirts, or shoes these days, because domestic manufacturers quickly lost access to capital. But it also means that industries going through what might be only a temporary low point can easily go to zero and never come back.

We view ourselves as the world’s good guys. When I talk to people about US free trade policy, one of the concerns is the effects that our policies have on workers in the third world. (This is not necessarily a well-informed concern. Back when he was interesting, Paul Krugman liked to point out that if you think a sweatshop sounds bad, you should ask yourself what kind of alternative employment made that sweatshop sound so good.)

In my readings, I did not see very many discussions at MITI about how their policies would affect Detroit. They seemed pretty concerned with how things would go in Nagoya. Detroit, they seem to have assumed, would take care of itself. (Or not.)

If you’re using traditional Ricardian thinking, MITI got it wrong: the global utility-maximizing move is to have everyone focus on whatever they’re currently good at. If you’re trying to gain an advantage over someone, the deadweight loss will hit you just as hard, or harder. That applies when comparative advantages are static, but not when they change over time. A change in comparative advantage is an abstraction. How it happens, concretely, is that a big new factory opens in one country and an older, smaller factory closes in a different, richer country.

Only if you’re willing to take actions that keep a relatively poor country relatively poorer than it otherwise would be can you run an effective industrial policy in a wealthy country. (Since poor countries have minimal domestic demand and cheap labor, their best option is to find products that are already in demand globally and could be made for less. In other words, they optimally compete head-to-head with incumbents.)

The idealized neoliberal view is that as countries get wealthier, they lose their comparative advantage in manufacturing but gain an advantage in services. Everyone loves American movies, right? Who cares if they don’t really want our cars? Movies are a pretty small business (the global box office is about $40bn/year, compared to around $4tr for the global auto industry. Auto revenues grow by several movie industries’ worth in a good year.). And while there are economies of scale, they tend to apply to things like plugging known acting talent together with well-known directors who can raise money from the right producers, etc. These don’t produce serious, globally-dominant industries with rising incremental returns on investment.They just give you Hollywood, Bollywood, and Nollywood; three small, separate local maxima.

Movies are an unfairly kind example to choose. Those we can export. American healthcare is mostly consumed and produced domestically, our retail industry is overwhelmingly focused on satisfying local demand, and our financial services industry also primarily matches local savers to local borrowers. Neoliberal policymakers will argue that as we deindustrialize, older workers will retrain. I’ll believe it when Cato fires their economics PhDs and replaces them with much more affordable former steelworkers.

Software is the big bet here. A US economy whose growth is dominated by global software giants, headquartered here, would indeed allow us to de-industrialize. In fact, it would more or less force it to happen. At scale, software companies produce high margins and don’t require much capital, so their ROIs are enormous. (And the big incremental expense that they do have is marketing, which is increasingly just revenue for a different software company.) As a result, they attract investment to the US — but since they’re high-margin businesses, they don’t produce much trade surplus relative to their profits. The result is a trade deficit that’s driven as much by supply of capital as it is by domestic demand for consumption.

This is a very big bet to make, and it’s a bet that we’re making blindly.

What we should explore instead is a policy of directly countering any country’s industrial policy to the extent that it’s designed to attack an industry the US still dominates that benefits from scale. Basically we’d go down the Made In China 2025 list and figure out what level of export subsidies and cheap loans would ensure that every single one of those products is Made In the USA by 2024. This may technically be against the rules, but those rules are hardly sacred.

The beauty of a policy like this is that it inverts the logic that the Miracle countries relied on. They knew that they could only earn high profits by exporting at scale; our policy just has to maintain profits at incrementally higher scales. Ideally, such a policy framework doesn’t ever actually get implemented. The point is that it’s cheaper for incumbents to stay on top than it is for challengers to get on top, so as long as incumbents commit to staying that way, challengers bother somebody else.[9]

To paraphrase The Princess Bride, we’ve fallen victim to one of the classic blunders: Never be the last to realize that you’re involved in a trade war in Asia.

The challenge America faces is that a free trade system optimizes on the margin, while industrial policy focuses on changing the overall balance of power. Once an industry moves to another country, it’s expensive to move it back, and the longer it grows the harder it gets. This means we have a comparative advantage when defending the industries we still have, but that we lose a little more of it every year. If we don’t take manufacturing exports seriously, someone else will.

Sources

- I started with Ha-Joon Chang’s Bad Samaritans, which is a great place to start if you’re a fan of free trade and love to argue. Chang’s book is mixed; there’s some good analysis, a little bit of “I got mine,” especially with respect to industrial espionage, and a couple dubious statistics.[10] But for an overview of the free trade skeptic’s case, it can’t be beat.

- A less partisan but more persuasive work is Joe Studwell’s How Asia Works. This one’s a masterpiece: in-depth profiles of both successes (South Korea) and failures (Malaysia), full of great lessons. My case studies draw heavily from this book. One of my favorite details, from a chapter on how a corrupt democratic process stymied the Philippines: they once had an election in which Marcos spent so much money buying votes that it literally triggered a balance of payments crisis.

- The Park Chung-Hee Era: I came away from this book with a lot more respect for Park, who was clearly one of the great statesmen of the twentieth century — a century that, considering the challenges it presented, was sadly lacking in greatness and statesmen.

- MITI and the Japanese Miracle. Like no other book I’ve read. It’s like Carlyle, but instead of the Great Man theory of history it’s the Great Bureaucracy theory.

- Alexander Hamilton’s Report on Manufactures. Sadly, there is not a hip-hop version available (“You say you fear a tariff/But the Brit is who you’ll scare if/You raise your nation’s output/and they learn too late what’s afoot.”)

- Friedrich List’s The National System of Political Economy. An economist who set out to refute Adam Smith. Prussia implemented this, the Meiji government in Japan cribbed from it, and Park Chung-Hee cribbed from them. He couldn’t have known that the ultimate result of his work was Volkswagen and BMW losing market share to Toyota, Honda, and Hyundai.

- Clashing Over Commerce is a wonderful history of trade policy. As is traditional in US history, there was a lively intellectual debate over the proper approach to trade policy, which had nothing whatsoever to do with how Congress ultimately behaved. In industrial policy terms, academia and the media manufactured soundbites, which were a low-margin, easily-copied product in which it’s hard to get a durable competitive advantage.